Industry Dynamics

Analysis of the development trend of Chinese hypoglycemic drug industry in 2018

一、 Global development trend of hypoglycemic drug market

(一)、Judgment of the development trend of clinical hypoglycemic drugs

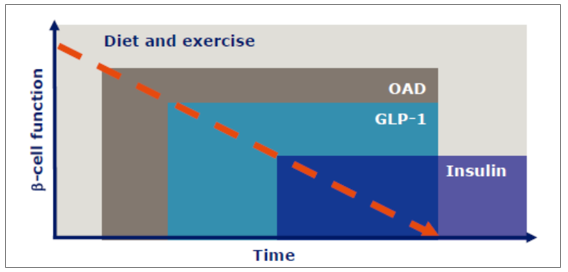

Depending on the different stages of diabetes (the ability of islet β cells to secrete insulin gradually decreases to zero), the current clinical drugs usually range from oral hypoglycemic drugs (OAD) to GLP-1 analog drugs to insulin, and usually combined according to the actual blood glucose control.

From the perspective of developed countries in Europe and the United States, the general judgment of the future development trend of clinical hypoglycemic drugs is as follows:

A、GLP-1 analogues are rising rapidly and have the most growing potential;

B、Insulin is still the last killer. As diabetes is a progressive disease in multiple pathogenesis, it is difficult to reverse its process at present, so the use of insulin is still a clinical rigid demand;

C、In the future, both the GLP-1 analog and insulin will coexist in the long term; and if viewed further term, given the delay of the disease progression, the market share of insulin may gradually shrink until a stable level in the future;

D、The oral medicine market has undergone great changes in the past decade, with the new generation of DPP-4 inhibitors becoming the main drug second only to metformin; and SGLT-2 inhibitors that have entered the market in the past five years are expected to become tomorrow's star.In addition, oral GLP-1 analogues have developed rapidly. If the clinical practical value (bioavailability, cost performance, etc.) can be confirmed, the pattern of hypoglycemic drugs market can be reconstructed.

Drug options at different stages of diabetes

Source: Public information collation

At the same time, the innovative drugs and generic drugs developed by domestic enterprises in these fields are also expected to be listed in the next few years. With the increase of market promotion and medical insurance support, the domestic hypoglycemic drug market is expected to accelerate the upgrading and replacement.

1、Analysis of domestic oral hypoglycemic drugs market

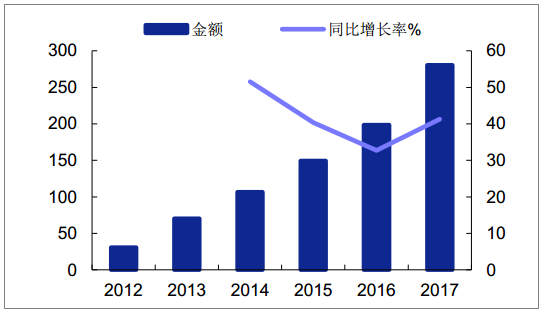

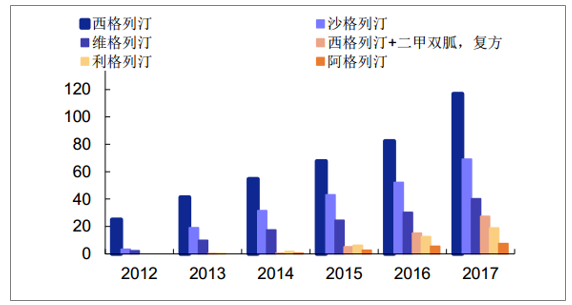

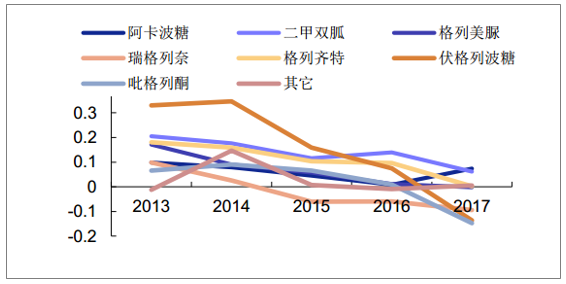

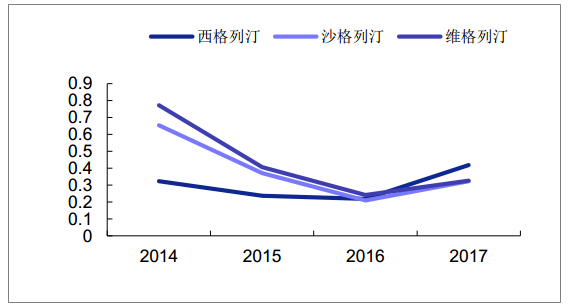

In the past few years, domestic DPP-4 drugs have grown steadily. In 2017, the growth showed an accelerated trend. The sales of PDB sample hospitals reached 280 million yuan, a year-on-year growth of 41%. It is estimated that the national market scale will be more than one billion yuan.Sigliptin and Sagliptin took the lead.Among other OAD drugs, both metformin and acabosose increased by about 7% (considering the increment is mainly from the grassroots, the national market size growth is higher than this); the market size of other oral hypoglycemic drugs in sample hospitals maintained stable or negative growth.The upgrading of the domestic OAD market is underway.

Market scale of Class DPP-4 drugs in domestic sample hospitals (one million yuan)

Source: Public information collation

Sales amount of Class DPP-4 drugs in domestic sample hospitals (one million yuan)

Source: Public information collation

Growth rate of oral hypoglycemic drugs sales in domestic sample hospitals

Source: Public information collation

Sales growth rate of Class DPP-4 drugs in domestic sample hospitals

Source: Public information collation

2、GLP-1 analogs are early in market introduction and competition is increasingly fierce

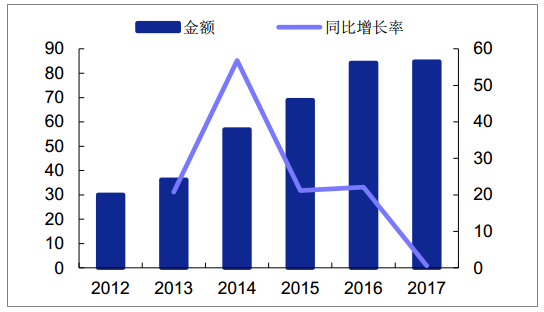

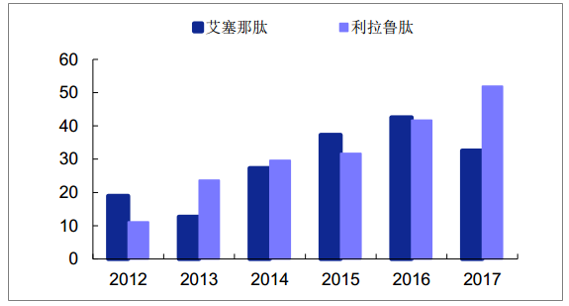

GLP-1 analogues are still imported early in China due to their extremely high prices.In 2017, the sales volume of PDB sample hospital was only 84 million yuan, and the estimated overall scale was only about 2 ~ and 300 million yuan.At present, only four GLP-1 drugs listed in China (short and long-term), rallutide, benallutide and rineptide have been listed in China.

Market scale of Class GLP-1 drugs in domestic sample hospitals (one million yuan)

Source: Public information collation

Sales amount of Class GLP-1 drugs in domestic sample hospitals (one million yuan)

Source: Public information collation

China's GLP-1 analogue market pattern

Source: Public information collation

In addition, two star GLP-1 drugs: Norde's Somalupin launched a phase 3 clinical trial in China in August 2017 and is expected to be approved in 2019; Lilly's taralupepin has applied to CDE for clinical exemption with international multicenter trial results containing Chinese data, and was included in the priority evaluation, which is expected to be approved by the end of 201 8.

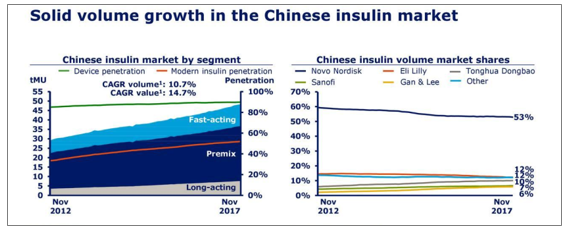

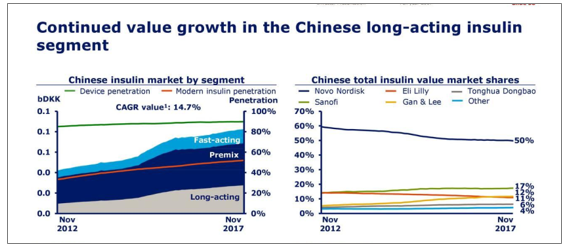

3、Domestic insulin has maintained rapid growth and been imported

In 2017 (in November), with sales of CAGR of 10.7% and 14.7%; insulin analog penetration accounted for more than 5 0% and sales of around 70%.In terms of market pattern, insulin sales ranked Novo Norde (53%), Lilly (12%), Tonghua Dongbao (10%), Sanofi (7%), Ganli (6%), and insulin sales ranked Novo Nord (50%), Sanofi (17%), Lilly (12%), Ganli (11%), Tonghua Dongbao (6%).

With Ganli Pharmaceutical, Tonghua Dongbao, Federal Pharmaceutical, various domestic insulin products have been marketed to the clinical practice, and the imported products are constantly replaced with their price and marketing advantages in the grassroots market

Insulin sales grew in China

Source: Public information collation

The growth of the insulin market in the Chinese market

Source: Public information collation

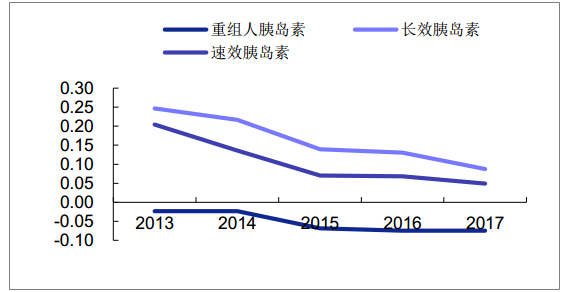

According to the data of sample hospitals, the overall market size of recombinant human insulin declined slightly in 2017, which is mainly related to the accelerated import substitution of national products with cheaper prices.The market size of insulin analogues maintained steady growth, with long-acting insulin sales up 8.7% and fast-acting insulin increasing 4.8%.

Market scale of different types of insulin in domestic sample hospitals (one million yuan)

Source: Public information collation

The growth rate of different types of insulin sales in domestic sample hospitals

Source: Public information collation

三、Current research and development progress of important hypoglycemic drugs in China

(一)、GLP-1 analogues

Among the hot development of GLP-1 analog drugs, the fastest progress in innovative drugs include: polyethylene glycol losenpeptide of Hausen Pharmaceutical has been reported, is expected to be approved this year, will become the second long-term in China GLP-1 drug; Paarogen's recombinant insulin secretin has also completed phase III clinical practice; rE4 of Shiqi Pharmaceutical is also in phase III clinical process.In addition, the oral GLP-1 analogues developed by Hengrui Pharmaceutical have also been declared for clinical practice, and are also a potential variety.

(二)、 SGLT-2 inhibitors

At present, 6 domestic innovative drugs can be found in the field of SGLT-2 inhibitors, among which the fastest net progress of Hengrui Pharmaceutical is in phase III clinic.SGLT-2 inhibitors listed abroad is not long (patent to expire after 2025), but the most potential in the future of OAD drugs, hengrui pharmaceutical through fast-follow strategy to follow up, rapid progress, is expected to market in the next 2 years, before a large number of generic drugs and imported drugs in domestic clinical promotion occupy first-mover advantage, is a potential blockbuster variety.

Progress in the research and development of innovative drugs related to SGLT-2 inhibitors in China

Source: Public information collation

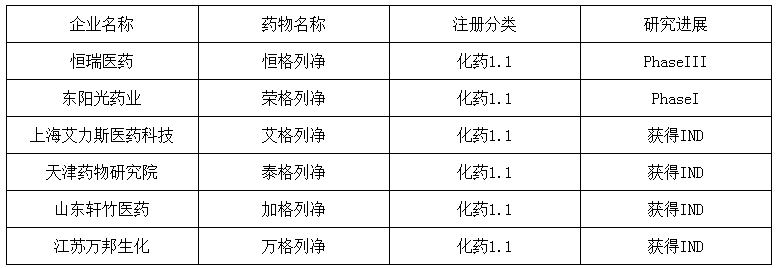

(三)、 DPP-4 inhibitors

The five varieties in the field of DPP-4 inhibitors have been overseas clinical overseas for a long time. After entering the national medical insurance directory in 2017, it can be predicted that these five varieties will lead the domestic DPP-4 drug market in the next few years.At the same time, in the next five years they will expire their Chinese patents (vigliptin 2019 patent expires, sagliptin 2021 patent expiration, sigliptin 2022 patent expiration, 2023 patent expiration), domestic enterprises currently cluster development, there will be a large number of domestic generic drugs listed, the competition will be extremely fierce.There are also a number of domestic enterprises developing DPP-4 inhibitor innovative drugs. In addition to the rapid progress, Ruigliptin and DBPR108 are expected to obtain certain market space before the large listing of generic drugs (but they also face competition from five imported products), leaving little room for subsequent innovative drugs.

For the record: the copyright of this article belongs to the original author, reprinted the article only for the purpose of spreading more information, if there is infringement, please contact us to modify or delete, thank you.